7 Steps to Become Debt Free in 2021

Solving debt-related issues is never easy. However, if you have a plan, it should be easier to concur! Here are steps to help you on your journey to becoming debt-free.

Do Your Accounting

That’s right, step 1 is to get your accounts in-check to work out how much debt you have accumulated. List each debt payment including the interest rates. Finalise this list by ranking each payment from highest interest to lowest to have a better understanding of your debt.

Analyse your Finances

Once you have figured out and have a better understanding of your debt, you need to work out how much you need to save monthly to pay off your debt.

A spreadsheet gives you autonomy to customise it to your needs and goals. It is simple and it works.

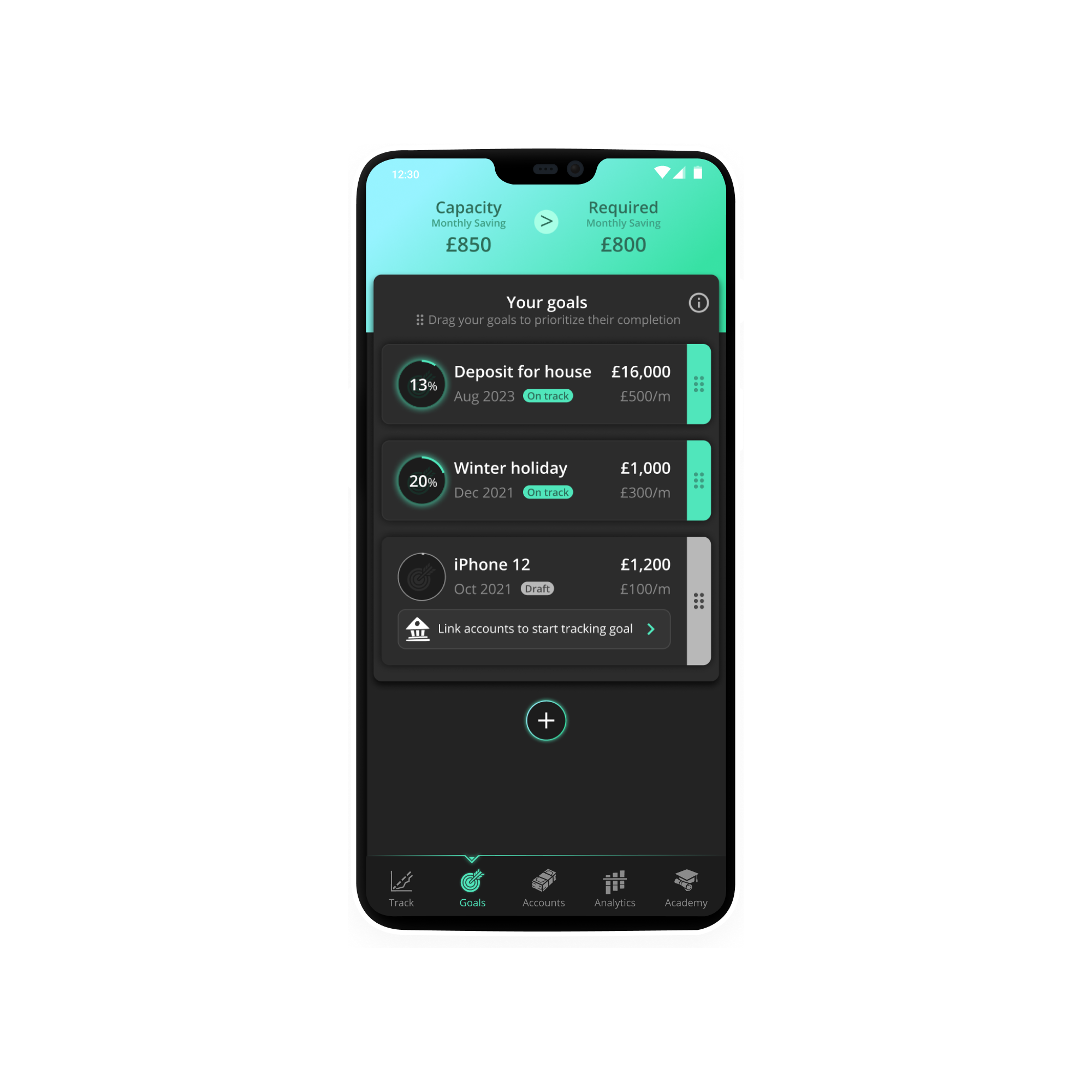

However, if you are not a fan of spreadsheets and cannot bring yourself to compute the numbers, you should download Nova!

Nova will put together a visual timeline to show you how and when you can become debt-free. Nova provides real time feedback on your spending patterns to improve your financial habits. Can’t save as much for the month? No worries! Nova will suggest adjusting your date of completion if you fail to reach your required saving for the month. Looking to become debt free and afford your first home at some point? The app allows you to prioritise your goals to see which order of completion you would like them to be in.

Get on the right track and get out of debt. Download Nova now.

Lifestyle Changes are a necessity

If you have spent more than you earn in the last six months, you are in dire need of a lifestyle revamp.

Your finances need a detox and your habits need some financial discipline. It’s time to track down unused subscriptions and unwanted direct debits. Cancel your Klarna account and chuck away your credit cards! Try some of these money-saving tips to get you started on your financial detox:

Challenge yourself to beat your best past self

If you already save a portion of your income, congratulations! You are on the right track to attain financial freedom. However, you should push yourself to do better and get out debt as soon as possible. Try to aim to save 20% of your income. Refer to the list of tips above to get your habits in check.

Did you know the average household can save over £350 annually by simply switching their energy supplier? If you are currently on your provider’s standard variable tariff, you are very likely to be missing out on better deals and bigger savings. Besides energy, you can save a lot of money on broadband alternatives too.

Find the best energy deal in your area right now by clicking the link here. For the best broadband deal in your area right now, click the link here.

Alternatively, download Cash Coach to challenge your best saving habits in order to save more money and find the best alternatives. The AI coach will help you through your objectives and even alert you on better energy and broadband deals if you are not already on it. Best of all, it is FREE. Try it now!

Consolidate debt

If you have a stable income and a good credit history, you may want to consider consolidating your debt.Consolidating debt usually involves taking out new credit in the form of a debt consolidation loan to pay off existing credit. You can also consolidate debt by transferring the balance to lower interest cards.

Check out our guide on the best 0% interest credit cards in the UK here.

Have a financial timeline

It is important to plan how long it will take to pay each source of debt. Be realistic.Working out how much money you have coming in and how much goes out (on essentials e.g. bills, groceries) monthly. Work this out to a ‘worst case scenario’ where you balance the lowest possible amount of income you are likely to have coming in against the largest outgoing you are likely to have. By doing this, you will know where you stand, and you will be in a positon to do something about it and achieve your goal of becoming debt-free.

Sticking Through It

This is the most important step. Sticking with your choices and plan. If you practice this, you will reach your goal of becoming debt-free.

I hope you find this guide informative. Remember, it is important to take control of your finances in order to stay out of debt and build wealth at the same time. That is why Nova is here to solve your worries. We promote smart spending habits, educate you on finance and push you to be the best version of yourself to achieve financial freedom.

Click the link below and download Nova now. With Nova, you are a step closer to becoming a millionaire!